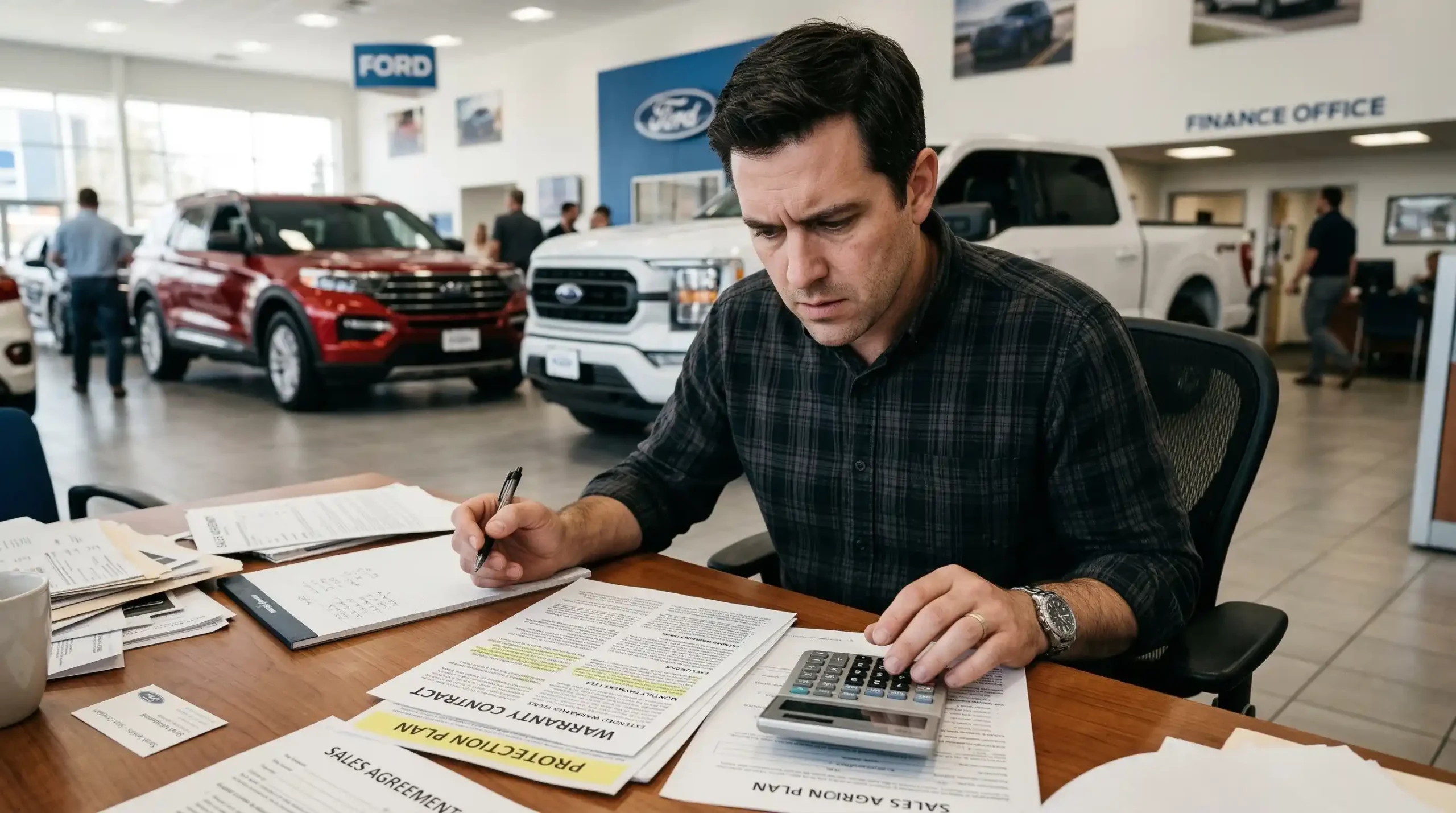

You just spent hours at the dealership. You are tired. The paperwork is almost done. Then the finance guy slides one more paper your way and says, “You want the extended warranty, right?” Most people say yes just to get out the door. I get it. I did the same thing once. But that moment can cost you way more than you think.

A dealership warranty sounds like a safety net. And sometimes it is. But there are real hidden costs baked into these plans that the salesperson will almost never bring up. Things like interest charges, deductibles, exclusions, and dealer markups can quietly drain your wallet over time.

In this blog, I want to walk you through the 5 highest hidden costs of dealership warranties so you know exactly what you are paying for before you sign anything.

What Is a Dealership Warranty and Why Does It Matter?

The Difference Between a Factory Warranty and a Dealer Warranty

When you buy a new car, it comes with a manufacturer’s warranty at no extra cost. This is the factory warranty. It is a promise from the carmaker to fix any defects for a set number of years or miles, whichever comes first. Most new cars get a bumper-to-bumper warranty of 3 years or 36,000 miles, and a powertrain warranty that lasts longer, often 5 years or 60,000 miles.

A dealership warranty is different. It is an optional product, sometimes called an extended warranty or vehicle service contract, that you buy separately. It is supposed to kick in after the factory coverage ends. The problem? The dealership often profits heavily from selling it to you.

According to the U.S. Federal Trade Commission (FTC), auto service contracts are optional products and can be expensive. They are often presented after you have already spent a long day at the dealership, making it easy to agree without thinking it through.

Why So Many Car Buyers End Up Paying More Than They Should

Here is something most people do not know. Dealers can mark up the price of a warranty plan however they want. There is no fixed price list. The dealer buys the plan for one price and then sells it to you for much more.

Honestly, the first time I bought a car, I had no idea I could even negotiate the warranty price. I thought the number on the paper was the number. It was not.

Industry data shows that dealer markups on extended warranties can range anywhere from 40% to 400%. That means a plan the dealer bought for $1,000 could be sold to you for as much as $5,000. Knowing this going in changes everything.

Hidden Cost #1: The Interest You Pay When You Roll It Into Your Loan

How Financing a Warranty Quietly Costs You More

One of the sneakiest hidden costs is the interest that builds up when you add a warranty to your car loan. The finance officer will often suggest, “Just roll it into your monthly payment.” It sounds harmless. It is not.

Say the warranty costs $2,400. If you finance it over 72 months at even a modest interest rate, you end up paying hundreds more in interest charges on top of the warranty price itself. A warranty that started at $2,400 can end up costing you $2,800 or more, just because of interest.

As reported by U.S. News & World Report, when a dealer breaks the warranty cost into monthly payments, it becomes easy to hide the true cost of the contract. They might say it is only $39.99 per month. Multiply that by 72 months and you have paid $2,879. That is the real number, not the small monthly figure they show you.

Also, adding a warranty to your loan raises your loan-to-value ratio. This means you may owe more on the car than it is actually worth. That is never a good position to be in.

The Smart Move: Pay Separately If You Decide to Buy

If you have decided a vehicle protection plan is right for you, pay for it separately. Do not let it get folded into your auto financing. This is a simple step that saves you from years of added interest on a product that may never even get used.

Also, remember you can negotiate. Most buyers do not know this, but the warranty price is not fixed. Those who push back and negotiate save an average of $325 on the price alone.

Hidden Cost #2: Deductibles and Copayments You Did Not Budget For

What Happens When You Actually Need to Use Your Warranty

Let’s say your engine light comes on. You take the car in. You assume the warranty will cover everything. Then the service advisor tells you there is a $200 deductible before coverage kicks in. That is a surprise no one wants.

Most dealership warranties include a deductible, which is an amount you must pay before the plan covers the rest. These deductibles typically range from $50 to several hundred dollars depending on the plan. Some plans offer a $0 deductible, but those usually cost more upfront.

There is also something called a copayment. This is a percentage of the repair cost you have to pay even after the deductible. If your copay is 20% and the repair bill is $600, you are still paying $120 out of pocket even after your coverage kicks in. These small amounts add up fast, especially on bigger repairs.

Per-Visit vs. Per-Repair Deductibles: Know the Difference

Some plans charge a deductible per visit to the shop. Others charge one for each individual repair done during that visit. If two things are fixed on the same day, a per-repair deductible plan could mean you pay the deductible twice.

I once looked at a warranty contract and saw the word “per occurrence” tucked into a footnote on page 8. That small phrase meant every single repair had its own cost to me. Easy to miss, costly to ignore.

Always ask specifically: “Is this a per-visit or per-repair deductible?” Get the answer in writing. It matters more than you think.

Hidden Cost #3: Diagnostic Fees and Unauthorized Repair Charges

Why Your Warranty Might Not Cover the Fee Before the Fix

Before any mechanic touches your car, they usually run a diagnosis to figure out what is wrong. This can cost $100 to $200 or more. Here is the thing: many warranty contracts do not cover diagnostic fees.

So even if the actual repair is 100% covered, you could still walk away paying for the diagnosis that found the problem. That is a hidden cost most people never see coming.

Some warranties also have an approved repair network, meaning you can only take your car to specific shops for the work to be covered. If you go to your regular mechanic who is not in the network, you may end up paying the full bill yourself. Or you might get only partial reimbursement.

What Happens When You Go Outside the Approved Network

Using a shop outside the approved service center list is called an unauthorized repair. Depending on your contract, this can mean your claim gets denied completely. Some plans require pre-approval before any repair work begins. If your mechanic starts fixing the car before getting that approval, the warranty company can refuse to pay.

Honestly, this is one of the most frustrating parts of dealing with a vehicle service contract. You are sitting in a repair shop, your car is broken, and you have to wait for someone from the warranty company to call back before anything gets done. I have heard this story from friends more than once.

Always read the section of your contract that explains where you can get repairs done. It is one of the most important parts of the whole document.

Hidden Cost #4: Coverage Exclusions That Leave You Paying Anyway

Why “Bumper-to-Bumper” Does Not Mean What You Think

The phrase bumper-to-bumper warranty sounds like it covers everything on the car. But it does not. Almost every contract has an exclusion list, and it can be surprisingly long.

Common exclusions include wear-and-tear items like brake pads, tires, wiper blades, and clutch discs. Damage from accidents, floods, or misuse is also not covered. Neither is routine maintenance like oil changes, tire rotations, or filters. So if you thought the warranty covered your brakes, think again.

Some plans have what is called an included components list instead of an exclusion list. This means only the specific parts listed are covered. Everything else is on you. These plans often sound great until you realize just how short the list really is.

The Exclusion List Is the Most Important Page in the Contract

When I was helping a family member buy a used car, we almost signed a warranty that excluded the entire electrical system. On a modern car, that is a huge deal. Infotainment screens, sensors, driver-assist features, all of it would have been out of pocket. We almost missed it.

Ask for the exclusion list before you agree to anything. Read it carefully. If the most common problems for your car’s make and model are on that list, the warranty coverage is not worth much to you at all.

According to a study by the FTC, buyers should always ask in writing what is covered and what is not before signing any auto service contract. That step alone can save you from a very expensive surprise.

Hidden Cost #5: The Markup You Pay Just Because You Did Not Negotiate

How Dealers Profit Big on Extended Warranties

This is the hidden cost that surprised me the most when I first learned about it. Dealerships do not just sell warranties. They make serious money on them. The finance and insurance (F&I) office at a dealership is one of the highest-profit departments in the whole building.

The dealer buys a warranty plan from the automaker or a third-party provider at a wholesale price. They then sell it to you at a much higher retail price. The difference, which is their profit, can be enormous. Industry insiders say dealer markups on extended warranties range from 40% to 400%.

Think about that. A plan that costs the dealer $1,000 might be offered to you for $4,000 or even $5,000. You would never know the difference unless you asked or compared prices elsewhere. This is not illegal. It is just how the business works. But it is something every car buyer should know.

Why Most Buyers Never Push Back on Warranty Pricing

By the time you get to the finance office, you are usually tired. You already spent hours negotiating the car price. The last thing you want is another negotiation. Dealers know this. That is exactly why the warranty pitch comes at the end.

But here is the thing: the warranty price is absolutely negotiable. Ask for a lower price. Get quotes from other dealerships. Look at third-party warranty providers too. A little bit of comparison shopping can save you hundreds of dollars.

Also, if you feel pressured, you can always walk away and buy a warranty later. Most extended warranty plans can be purchased after the sale, not just at the dealership on signing day. Do not let anyone tell you otherwise.

Is a Dealership Warranty Worth It at All?

When It Makes Sense and When It Does Not

To be fair, a dealership warranty is not always a bad idea. If you are buying a car with high average repair costs, like certain European luxury brands, having some coverage can make sense. Statistically, owners of less reliable vehicles use their warranties far more. BMW owners, for example, use their warranty coverage at a much higher rate than Honda or Toyota owners.

But for a reliable make and model with low repair history, you might be better off putting that $1,500 or $2,000 into a savings account as your own personal emergency repair fund. That way the money is yours to keep if nothing goes wrong.

What to Do Before You Sign Any Warranty Contract

Before agreeing to any vehicle protection plan, ask these questions: What is the deductible? Where can I get repairs done? What is on the exclusion list? Can I transfer this if I sell the car? Is the price negotiable?

Get every answer in writing. Do not rely on what someone tells you verbally in the moment. A warranty contract is a legal document, and what is written in it is what matters when you have a broken car and a repair bill in your hand.

Conclusion

A dealership warranty can sound like a great deal. But behind the surface, there are real hidden costs that can make it far more expensive than it first appears. From interest charges on financed warranties to diagnostic fees, deductibles, coverage exclusions, and massive dealer markups, the total you pay can be much more than what you expected.

The good news? Now you know. You can walk into that finance office prepared, ask the right questions, negotiate the price, and make a smart decision based on real information rather than end-of-day pressure.

Have you ever bought an extended warranty and felt like you were not told the full story? I would love to hear your experience in the comments below.

Frequently Asked Questions (FAQs)

What are the most common hidden costs of a dealership warranty?

The most common hidden costs include deductibles you pay before coverage starts, diagnostic fees that are often not covered, interest charges if you finance the warranty, coverage exclusions for wear-and-tear items, and the dealer markup baked into the sale price. Together, these can add hundreds or even thousands of dollars to what you actually spend.

Can I negotiate the price of a dealership warranty?

Yes, absolutely. The price of a dealership warranty is not fixed. Dealers mark up warranty plans significantly, which means there is room to negotiate. Buyers who push back on price save an average of a few hundred dollars. You can also compare prices with other dealerships or look at third-party warranty providers to get a better deal.

What is not covered by a dealership extended warranty?

Most vehicle service contracts exclude routine maintenance items like oil changes, brake pads, tires, and wiper blades. They also exclude damage from accidents, flooding, or improper use. Some contracts exclude entire systems like the electrical system or infotainment components. Always ask for the full exclusion list before signing.

Is it better to get a dealership warranty or a third-party warranty?

A manufacturer-backed warranty from the dealership usually allows you to get repairs at any franchised dealership, which is convenient. Third-party warranties can be cheaper and more flexible, but they sometimes require you to pay upfront and get reimbursed later. Compare coverage, price, and approved repair networks before deciding which is better for your situation.

Should I roll my warranty into my car loan?

Generally, no. Rolling your extended warranty into your car loan means you pay interest on it for years. This adds to the total cost significantly. It also raises your loan-to-value ratio, which means you could owe more on the car than it is worth. If you decide to buy a warranty, it is smarter to pay for it separately as a one-time payment.